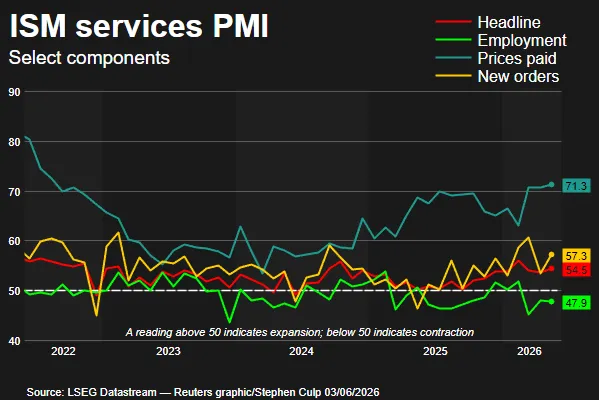

The Services PMI surged by a significant 0.9 percentage points to 54.5 in May, signaling growth acceleration. Businesses responded to supply chain pressures by rapidly increasing new order intake.

Businesses in the U.S. services sector accelerated their pace in May, driven by proactive ordering and inventory replenishment amidst concerns over supply chain disruptions caused by the ongoing conflict in the Middle East.

Related ↗IDR survey reveals UK pay settlements remain steady at 3.5% for a second consecutive month.A surge in prices paid by US services firms reached a near-four-year high in May, according to the Institute for Supply Management's latest survey. Petroleum-related costs skyrocketed, marking a significant departure from April's data, where such concerns were notably absent among ISM respondents on Wednesday.

A three-month conflict between the US and Iran has caused significant disruptions to commodity supplies, leading to increased costs for essential items like energy, aluminum and fertilizers.

Read next ↗Gulf region stock markets decline sharply today suddenly.The Federal Reserve's Beige Book report on Wednesday highlighted accelerating growth in the US services sector in May. Prices rose at a moderate to strong pace overall, driven primarily by energy-related costs stemming from the conflict in the Middle East, which also affected shipping, packaging, groceries and fertilizer.

Markets anticipate that the Federal Reserve will maintain current interest rates through next year's end.

Economic growth remains robust despite escalating inflation concerns, according to Priscilla Thiagamoorthy, a senior economist at BMO Capital Markets, who notes this trend may influence the Federal Reserve's decision-making process.

The non-manufacturing purchasing managers index surged to 54.5 in May, marking a significant jump from April's 53.6. Economists had predicted a PMI reading of 53.8, according to polls. This uptick signals growth within the services sector, which drives over two-thirds of U.S. economic activity.

Manufacturing momentum is reflected in the services PMI, which shows a similar uptick according to ISM data released recently. A total of seventeen sectors experienced growth in April, with notable increases in wholesale trade, construction, public administration, accommodation, food services, utilities and retail trade industries. Meanwhile, real estate, rental and leasing saw a decline.

Businesses participating in the ISM survey expressed concerns over escalating inflation and burgeoning supply chain issues. Educational service providers noted a growing scarcity of essential resources, including construction materials and computer hardware such as laptops and tablets.

Businesses in the accommodation and food services sector report that suppliers from various industries are attempting to shift higher fuel charges and rising production costs onto them, particularly for resin-based goods. This will likely result in substantial expense hikes affecting these businesses by the end of June at the latest and certainly by September.

Capital expenditure for energy projects remains stalled due to shifting macroeconomic conditions, while data centers fuel a surge in demand, thereby limiting supply in the piping sector.

Wall Street stocks declined following their recent surge, while the dollar strengthened against a composite currency index. Meanwhile, US Treasury bond yields increased sharply.

14Stocks Rise Quickly.

New orders for service-based businesses surged significantly in April, with a notable increase to 57.3 from 53.5 previously recorded. Meanwhile, inventory levels within the services sector skyrocketed to an impressive 62.5, marking the highest reading since May 2010. This upward trend comes after four consecutive quarters of declining business inventories, a period not seen since the Great Recession.

The ISM services business survey committee's chair, Steve Miller, views the surge in inventories with a cautious eye, attributing it to respondents' optimism about sustained business activity despite escalating costs. The inventory sentiment index rose by just 0.1 percentage point, a relatively modest increase. Meanwhile, growth in backlog orders and exports has begun to stall.

Business input prices surged to a record high of 71.3, surpassing August 2022 levels, following a slight dip from 70.7 in the previous month. This uptick suggests that the oil price shock will have a lasting impact on service industries. Meanwhile, inflation accelerated at its fastest rate in three years during April, according to recent government data.

The pace of supplier deliveries slowed slightly to a still-elevated 55.2 in April, down from 56.8. This reading above 50 suggests that deliveries are actually slowing, contrary to expectations. The surge in services PMI is likely due to an economy gaining momentum and rising demand. Strained supply chains, however, are the underlying cause of longer delivery times in this case.

Electronic devices and computer parts faced a persistent shortage of inventory.

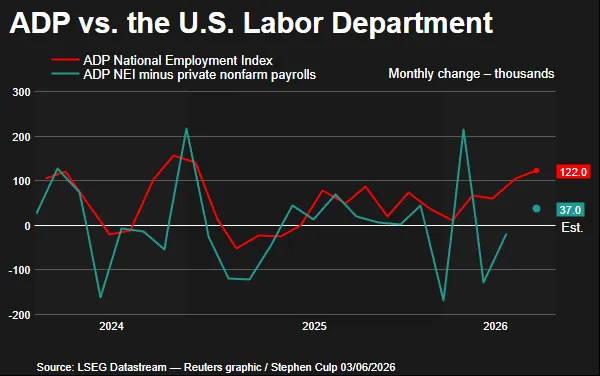

Employment numbers in the services sector continued to disappoint, with many companies opting for hiring freezes or failing to fill vacant roles. Meanwhile, new data released on Wednesday revealed that private employers added 122,000 jobs in May, following an increase of 105,000 positions in April.

Contrary to the Beige Book's findings, most regions reported a sluggish hiring climate, characterized by few job openings and limited turnover. Hiring was concentrated in essential positions or replacing departing employees.

Economists generally consider the labor market to be in a state of stability following last year's volatility caused by tariffs.

The ADP report, a collaborative effort with the Stanford Digital Economy Lab, precedes the highly anticipated Bureau of Labor Statistics' release on Friday by providing initial insights into the labor market. Its track record suggests it often falls short in accurately predicting the BLS's more comprehensive private payrolls forecast.

Tuesday's release of the Job Openings and Labor Turnover Survey revealed a significant drop in layoffs, while hiring also slowed down, contributing to the reported addition of 115,000 jobs in the nonfarm payrolls for April.

According to a survey, economists anticipate a significant increase in payrolls for May, with an estimated rise of 85,000 jobs. Meanwhile, the unemployment rate is expected to remain unchanged at 4.3% throughout this period.

Recent data from key forecasting tools has been disappointing, with indicators like NFIB hiring intentions indexes and regional Fed surveys showing a decline in recent months. The Conference Board's job availability differential survey also indicates a weakening trend. This lack of convincing evidence suggests the labor market may not be regaining momentum as quickly as expected.