A $1.5 million settlement between Elon Musk and the SEC has been reached without any evidence of impropriety. The SEC's lawsuit against Musk was allegedly driven by a perceived political agenda, he asserts.

A settlement between Elon Musk and the U.S. Securities and Exchange Commission has been defended as fair, with both parties claiming it represents a genuine compromise rather than a collusive agreement, despite concerns raised by the presiding judge.

Related ↗British companies halt recruitment amid Iran conflict impact, REC research indicates.A mutually beneficial agreement has been reached between Musk and the SEC, with both parties conceding concessions while securing benefits, as revealed in a Monday night filing in the Washington, D.C., federal court.

The SEC filed an additional document on Monday, revealing that under the agreed-upon terms, Musk will be allowed to dispute the allegations publicly, in line with new guidelines for settling enforcement cases.

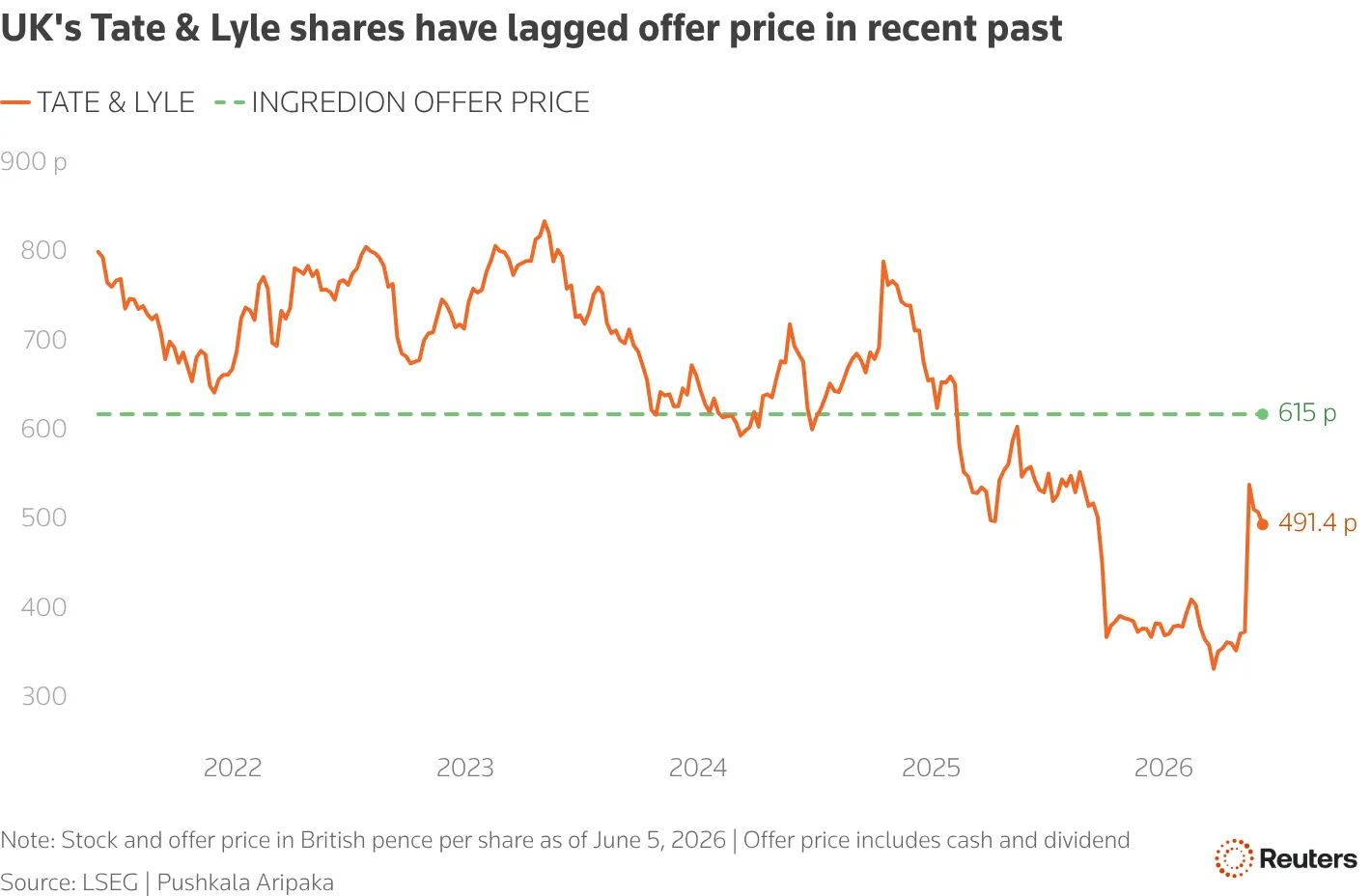

Read next ↗Tate & Lyle accepts a £2.7 billion all-cash acquisition from Ingredion.A trust bearing Elon Musk's name must pay a $1.5 million fine as part of the settlement, addressing allegations that he delayed disclosure of his Twitter stock purchases by 11 days in March and April 2022, thereby acquiring shares at discounted rates ahead of investor awareness.

The Twitter acquisition delay was attributed to an unintentional oversight by Musk, who subsequently acquired the platform for a staggering $44 billion in October 2022, rebranding it as X.

U.S. District Judge Sparkle Sooknanan expressed skepticism at a May 13 hearing about the fairness of the settlement terms, pointing out that the SEC's fine targeted the trust rather than Musk personally and recovered only 1% of his $150 million in allegedly misappropriated funds.

The settlement's legitimacy will be scrutinized to ensure it aligns with the public's best interests, untainted by any corrupt influences.

Elon Musk settlement between Elon Musk and the U.S. Securities and Exchange Commission has been defended as fair, with both parties claiming it represents a genuine compromise rather than a collusive agreement, despite concerns raised by the presiding judge.

The trust bearing Elon Musk's name must pay a $1.5 million fine as part of the settlement, addressing allegations that he delayed disclosure of his Twitter stock purchases by 11 days in March and April 2022, thereby acquiring shares at discounted rates ahead of investor awareness.

11Public interest protected through settlement agreement.

The settlement was reached without any indication of improper collusion, according to Musk and the SEC's statements.

The Securities and Exchange Commission imposed a record-breaking fine of $1.5 million, surpassing the previous high of $950,000, as part of a settlement agreement mirroring its approach to similar cases recently.

An injunction in place effectively constrains Musk's actions when carried out through the Revocable Trust, a financial entity reportedly utilized by him to oversee significant portions of his assets, according to the SEC's statement.

Elon Musk stated that he would have likely emerged victorious in court, particularly regarding the SEC's alleged selective targeting of his freedom of expression.

The hefty fine imposed on Carl Icahn stands out, considering the $500,000 penalty levied against him in 2024 for more egregious behavior, where he concealed his majority stake in Icahn Enterprises (IEP.O) for over three years to secure billions of dollars in personal loans. A secondary $1.5 million fine was also incurred by Icahn Enterprises.

Tesla's CEO, Elon Musk, described the deal as a quintessential example of a mutually beneficial concession involving a significant financial settlement.

Formerly, Elon Musk served as an advisor to Republican President Donald Trump. A lawsuit was filed against Musk by the SEC just prior to Democratic President Joe Biden's departure from the White House.

Under new leadership, SEC Chair Paul Atkins is reorienting the agency's focus amidst reduced corporate oversight efforts by the Trump administration.

Margaret Ryan, former head of SEC enforcement, unexpectedly departed in March after a tenure of only six months amidst disagreements with senior SEC officials regarding enforcement policies.