A top Deutsche Bank executive stated on Wednesday that their institution will not resort to aggressive marketing tactics to lure new clients, despite increasing rivalry from JPMorgan's growing presence in the German market for retail banking services.

Deutsche Bank's finance chief stated on Wednesday that the German lender won't engage in aggressive marketing tactics to lure new clients, despite intensified competition from US-based JPMorgan, which is expanding its presence in Europe's largest economy with growing momentum.

Related ↗British companies halt recruitment amid Iran conflict impact, REC research indicates.Deutsche Bank's Chief Financial Officer Raja Akram stated at a financial gathering that stiff competition is nothing unusual in this market.

In April, JPMorgan launched its Chase digital retail bank in Germany, introducing an attractive 4% deposit rate for newcomers that lasts for exactly four months.

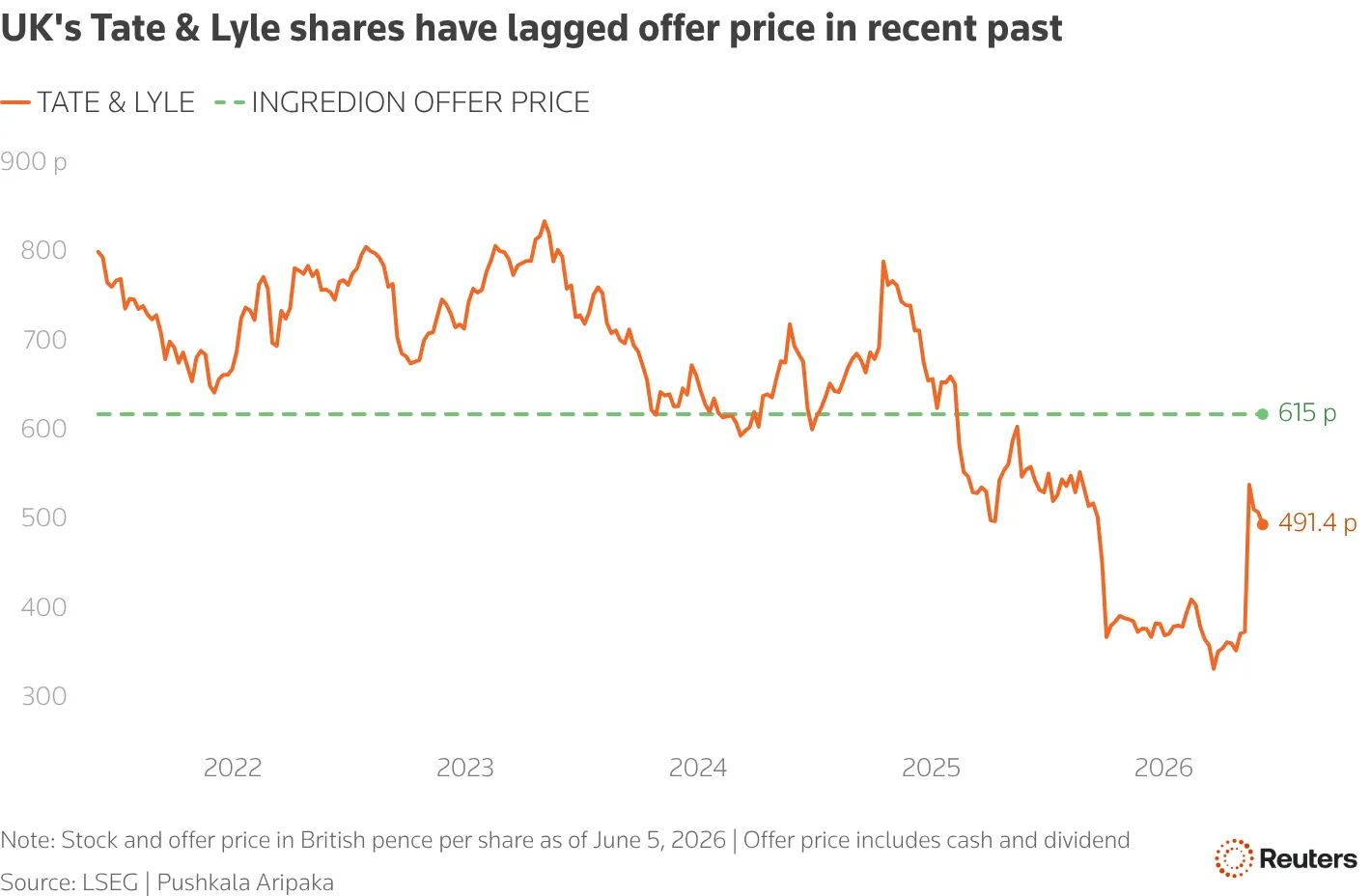

Read next ↗Tate & Lyle accepts a £2.7 billion all-cash acquisition from Ingredion.Akram stated that competitors are launching extremely competitive offers, a strategy their bank chooses not to replicate.

Deutsche Bank's Postbank brand retaliates with a competitive offer: a 3.2% promotional rate for new clients on deposits for six months. Meanwhile, its smaller subsidiary Norisbank sweetens the deal with a 4% rate and a one-time bonus to switch from another bank immediately.

Our focus is on deepening existing relationships, leveraging our established client base to grow deposits and expand our market share in Germany.

The German market for retail banking services presents a highly competitive landscape, with numerous lenders vying for a significant share of the country's affluent and sizable population.

Entering the German retail banking market, a US bank's potential impact raises concerns about which institution would be more vulnerable to losing customer deposits. Deutsche Bank, with its traditional relationship-driven approach, might struggle against a single-product digital bank that initially attracts customers solely through competitive interest rates, only to lose them once those rates expire.